|

|

Upfront Briefing

FDA is floating a pathway to cut time to first-in-human trials — framed as part of budget-driven reforms. Translation: less waiting, more dosing.

On the company tape, Sanofi posted Phase 2 respiratory wins for lunsekimig while Takeda handed DNL593 back to Denali, reinforcing how quickly platform narratives can sharpen or wobble once capital allocation and partnering decisions hit.

Tape Action

| Instrument |

Last close |

1D % |

YTD % |

| S&P 500 |

6,611.8 |

+0.4% |

(3.6%) |

| Nasdaq 100 |

24,192.2 |

+0.6% |

(4.0%) |

| Russell 2000 |

2,540.6 |

+0.4% |

+1.3% |

| Healthcare (XLV) |

146.1 |

(0.4%) |

(5.7%) |

| Biotech (XBI) |

128.8 |

(0.1%) |

+6.0% |

| Nasdaq Biotech (NBI) |

5,826.7 |

(0.4%) |

+2.1% |

| Clinical Trials (BBC) |

42.8 |

+0.6% |

+9.3% |

|

- Index tape was modestly risk-on: the Nasdaq 100 rose +0.6% and the S&P 500 added +0.4%, suggesting investors were still willing to add growth exposure despite macro noise.

- Healthcare lagged again (XLV (0.4%)), while biotech was mixed: XBI slipped just (0.1%) versus NBI (0.4%), which reads more like rotation away from large-cap biotech than a broad sector de-risking.

- Small caps still held in (Russell 2000 +0.4%), consistent with a tape that remains open to selective higher-beta exposure rather than hiding purely in defensives.

- Market data: U.S. close Mon 06-Apr-2026.

The Big 3

|

1

|

FDA proposes pathway to cut time to first-in-human trials

|

- FDA’s FY2027 budget request proposes an optional alternative to the traditional IND process aimed at getting sponsors into first-in-human studies faster, with the pitch centered on lower cost and less delay for early development.

- Why it matters: For early-stage biotech, time to first patient is not just an operational metric — it directly affects cash burn, catalyst timing and financing leverage. If FDA eventually implements a credible faster-entry pathway without raising downstream regulatory risk, it could pull human proof-of-biology readouts forward and improve the capital efficiency of pre-proof companies. The caveat: this is still a proposal, not a rule change, so investors should treat it as a potential framework shift rather than an immediate modeling input.

- Source: BioCentury

- More: BioPharma Dive

|

|

2

|

Sanofi’s lunsekimig hits Phase 2 endpoints in asthma and CRSwNP

|

- Sanofi said lunsekimig met primary and key secondary endpoints in the AIRCULES Phase 2b asthma study and the DUET Phase 2a CRSwNP study, while the exploratory VELVET Phase 2b study in atopic dermatitis missed its primary endpoint. Lunsekimig is a pentavalent bispecific Nanobody targeting TSLP and IL-13.

- Why it matters: The investor readthrough is mechanism validation in respiratory disease, not a clean platform win everywhere. Positive asthma and CRSwNP data support the idea that dual blockade of an upstream initiator (TSLP) and downstream effector (IL-13) can translate into meaningful efficacy, which helps justify Sanofi’s broader respiratory ambition and could raise the strategic value of differentiated multispecific immunology assets. The AD miss matters too: it narrows where investors should underwrite the molecule and argues against giving full “pipeline-in-a-product” credit.

- Source: Sanofi PR

- More: GlobeNewswire mirror

|

|

3

|

Takeda returns DNL593 to Denali as neuro partnership unwinds

|

- Takeda is ending its collaboration with Denali and returning rights to DNL593, a progranulin replacement therapy being developed for frontotemporal dementia. Reports say the move was strategic rather than driven by safety or efficacy concerns.

- Why it matters: In biotech, partnership reversals are never just administrative. Even when framed as “strategic,” a return of rights removes external validation and shifts both cost burden and narrative risk back to the biotech. For Denali, investors now have to re-underwrite DNL593 on standalone merit; for the sector, it is a reminder that large-pharma appetite in neuro remains selective, especially for programs that still need substantial clinical de-risking.

- Source: Fierce Biotech

|

Everything Else that broke

- Hims & Hers says limited data stolen in social engineering attack. — BioPharma Dive

- Neuronetics shareholder urges strategic review, including TMS sale. — PR

- Akeso shares updated cadonilimab combo data in resistant NSCLC. — PR

- Renovare launches, ties collaboration to up to $33.5M ARPA-H. — PR

- Biodesix previews AACR 2026 posters on diagnostics pipeline. — PR

- BioWorld: Regulatory actions roundup for April 6, 2026. — BioWorld

Deal Flow

| BioBucks 2026 Deal Trackers • Updated weekly ⬇️

|

M&A / BD&L

-

Neurocrine to buy Soleno for $2.9B, targeting Prader-Willi. — BioCentury

-

Takeda returns DNL593 to Denali as part of neuro restructuring. — Fierce Biotech

-

Ascendis gets orphan exclusivity and launches YUVIWEL in the U.S. — PR

VC / Private Financings

- Stipple Bio emerged from stealth with an oversubscribed $100M Series A; co-led by RA Capital, a16z Bio+Health and Nextech Invest, joined by Emerson Collective Investments, GV, LoLa Capital Partners and GordonMD Global Investments. — PR

- Syneron Bio closed a $150M Series B to advance its macrocyclic peptide platform; led by an international life-science fund, with Decheng Capital and CDH VGC as co-leads, and backing from ADIA, True Light Capital, Qiming Venture Partners and AstraZeneca. — PR

IPOs / Follow-Ons

- Korsana heads to NASDAQ via merger, BioCentury reports. — BioCentury

Things that make you go hmmm ...

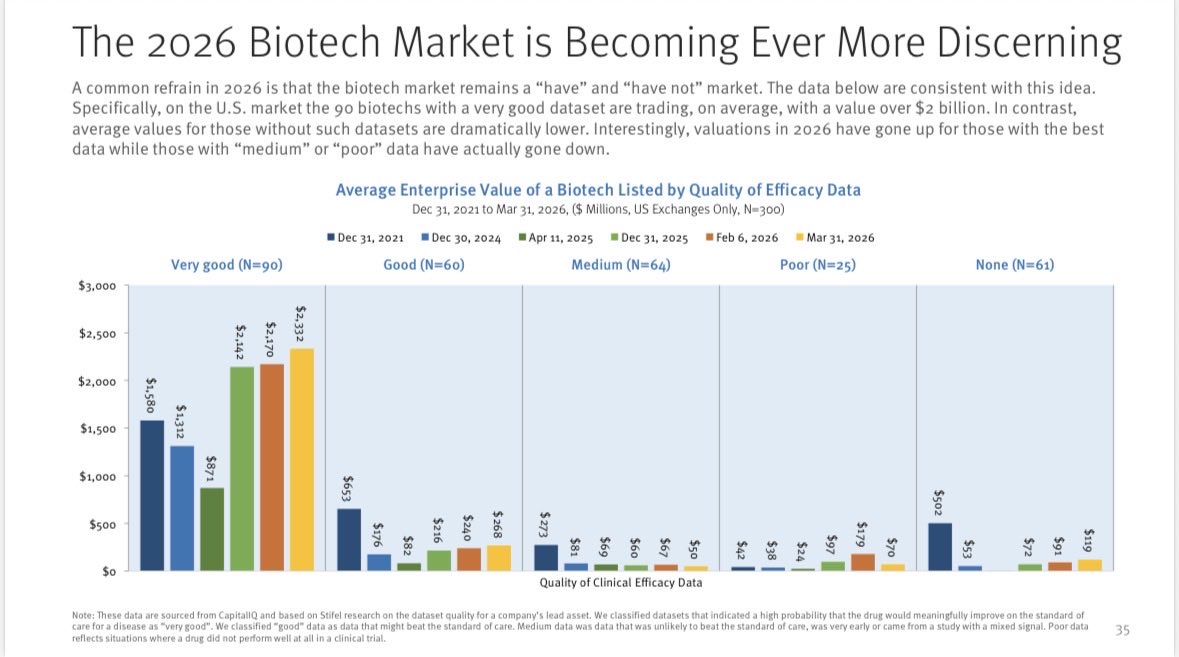

Clinical data quality vs. valuation Source: Stifel

|

|

That’s it for today — may your endpoints be met and your timelines pulled forward (preferably by FDA, not by your board). See you tomorrow. BioBucks Team

|

|

|