Upfront Briefing

Gilead’s back in the shopping aisle: a Tubulis takeout worth up to $5B to deepen its ADC bench beyond Trodelvy.

Meanwhile, policy put Humira on the TrumpRx list alongside cheaper biosimilars — and deal filings around Merck’s Terns buy added some spicy color on bid dynamics (read: price).

Tape Action

| Instrument |

Last close |

1D % |

YTD % |

| S&P 500 |

6,616.9 |

+0.1% |

(3.3%) |

| Nasdaq 100 |

24,202.4 |

0.0% |

(5.0%) |

| Russell 2000 |

2,544.9 |

+0.2% |

+1.8% |

| Healthcare (XLV) |

146.6 |

+0.2% |

(5.3%) |

| Biotech (XBI) |

128.9 |

0.0% |

+1.9% |

| Nasdaq Biotech (NBI) |

5,814.2 |

(0.2%) |

(2.2%) |

| Clinical Trials (BBC) |

43.1 |

+0.7% |

+11.6% |

|

- U.S. tape finished mixed after a volatile session tied to Iran / Strait of Hormuz headlines: the S&P 500 still closed modestly higher (+0.1%) and the Russell 2000 added +0.2%, suggesting investors were willing to buy the late-day rebound rather than de-risk wholesale.

- Biotech lagged broader risk appetite: XBI was essentially flat (+0.04%) while NBI fell (0.4%), which reads less like broad capitulation and more like continued selectivity around large-cap biotech and earnings-quality names.

- Healthcare held in better than biotech, with XLV up +0.2%, reinforcing the market’s current preference for defensiveness and cash-flow durability even as investors still selectively added small-cap beta.

- Market data: U.S. close Tue 07-Apr-2026.

The Big 3

|

1

|

Gilead to buy Tubulis in ADC deal worth up to $5B

|

- Gilead agreed to acquire Tubulis for $3.15B upfront plus up to $1.85B in milestones, adding next-generation ADC capability and two key assets: TUB-040, already in Phase 1b/2 in ovarian and lung cancer, and earlier-stage TUB-030.

- Why it matters: Gilead is paying real money for a clinical-stage payload/linker toolkit and an asset base that can matter beyond Trodelvy. For investors, the readthrough is that differentiated ADC engineering still commands scarcity value — especially when attached to programs already moving toward later-stage development — and that large-cap pharma remains willing to pay up for oncology platform depth rather than wait for fully de-risked assets.

- Source: BioCentury

|

|

2

|

White House adds AbbVie's Humira to TrumpRx list

|

- The White House added AbbVie's Humira to TrumpRx alongside cheaper biosimilars. The move spotlights public-channel pricing pressure in the Humira market.

- Why it matters: Humira is already a melting-ice-cube franchise, so the key investor question is not whether public scrutiny hurts sentiment — it is whether channel pressure accelerates price compression faster than AbbVie can manage mix, rebates and switch dynamics. Putting Humira on TrumpRx sharpens attention on the pace of residual cash-flow erosion in a franchise the market already treats as ex-growth, while also reminding investors that policy pressure can still drag legacy blockbuster math lower even late in the loss-of-exclusivity curve.

-

Source:

Endpoints

|

|

3

|

Filings: Terns accepted lower Merck bid after updated data review

|

-

Updated merger filings show Terns previously received higher offers, including proposals at up to $61/share and a CVR structure, before bidders revisited valuation after additional diligence on TERN-701 and Merck ultimately won with a $53/share takeout.

-

Why it matters:

The investor signal is not simply “there was a higher bid.” It is that incremental clinical diligence changed how buyers underwrote TERN-701’s differentiation versus Scemblix, which in turn reset price. That is a useful reminder that in competitive biotech auctions, valuation can compress quickly when updated datasets make a lead asset look less cleanly de-risked than headline ASH enthusiasm first implied.

-

Source:

BioPharma Dive

|

Everything Else that broke

- Novo Nordisk launches high-dose Wegovy. — STAT

- Study: $35 monthly insulin cap increased patient access. — Endpoints

- FDA approves and launch begins for generic nintedanib capsules. — PR

- BioCentury: Precision mTOR targeting in TSC epilepsy. — BioCentury

- Endpoints: What’s familiar in health tech’s Q1 funding totals. — Endpoints

Deal Flow

| BioBucks 2026 Deal Trackers • Updated weekly ⬇️

|

M&A / BD&L

-

Gilead to buy Tubulis in ADC deal worth up to $5B, adding depth beyond Trodelvy. — BioCentury

- Filings: Terns rebuffed a higher bid before Merck deal. — BioPharma Dive

- Lilly pays AC Immune CHF10M (~$12.5M) to expand Alzheimer’s collaboration as a candidate moves closer to the clinic. — Fierce Biotech

- Novonesis buys Southeast Asia production facility. — PR

- ATLATL and Daiichi Sankyo sign APAC biotech innovation deal. — PR

- RoosterBio, MineBio partner in China on MSC, exosome bioprocessing. — PR

VC / Private Financings

- Kytopen disclosed a Series B financing led by Telegraph Hill Partners, with participation from existing investors, to support commercial expansion of its non-viral cell-engineering platform. — PR

IPOs / Follow-Ons

- Daré Biosciences opens public offering aimed at retail. — BioSpace

Things that make you go hmmm ...

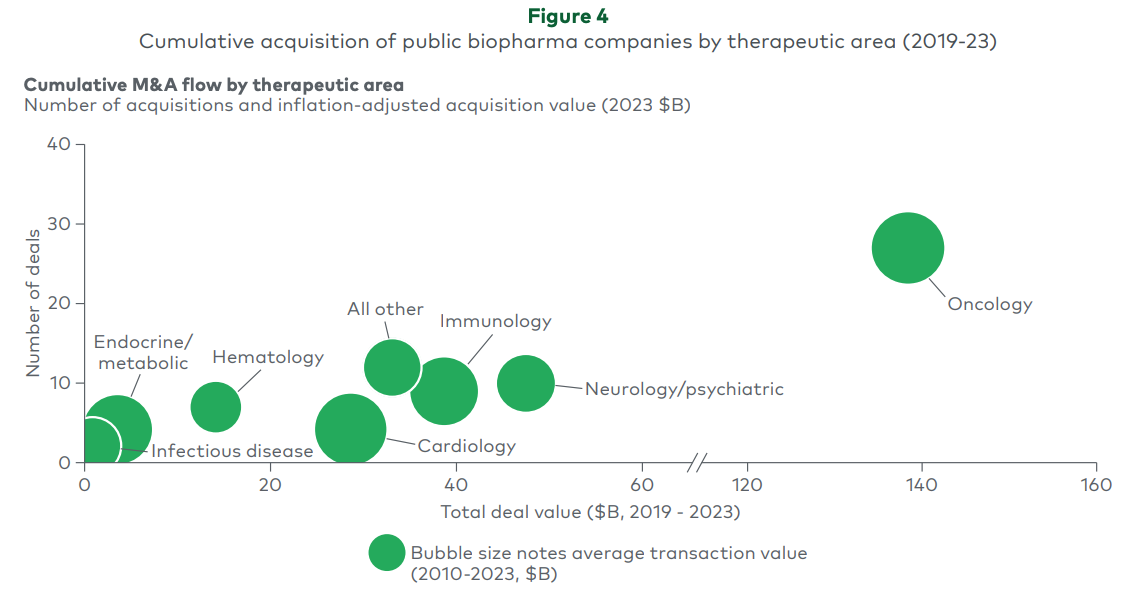

Oncology has taken the majority of M&A dollars. — Source: L.E.K.

Academic Corner - Zodasiran for cholesterol and triglyceride lowering in patients with hyperlipidemia: final report of phase 1 basket trial. — Nature Medicine

|